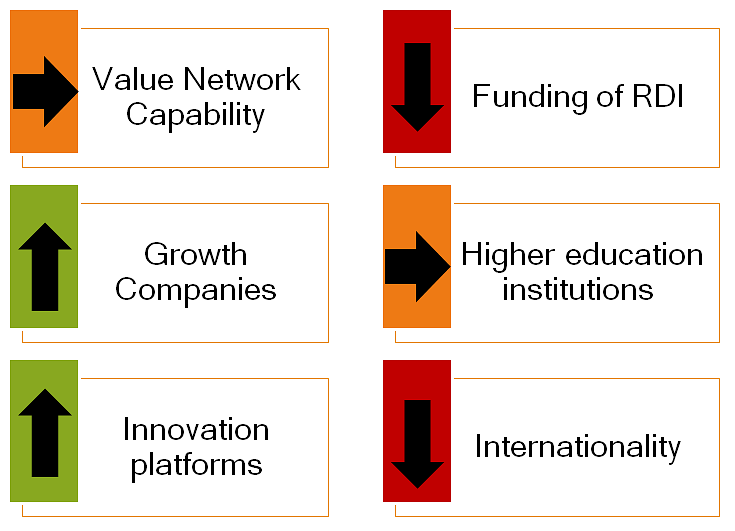

This is the fourth Situational Picture of Innovation made in the Tampere Region. The first Situational Picture was published in 2013 and the operating model has been developed each year since that time. The Situational Pictures identify not only the Tampere region's strengths, but also its weaknesses and challenges. The Situational Picture interprets and compiles data on six areas:

- Value Network Capability (previously business environment)

- Higher education institutions

- Internationality

- Growth companies

- Innovation platforms

- RDI funding

The Tampere Region's performance and competitiveness has fallen slightly over the past few years. The economic structure has been undergoing change for a long period of time and the reformed business sector has not yet been able to fill in the gaps left by old structures. The challenges facing industry and soft export growth over the past few years have dealt a serious blow to the Tampere Region's competitiveness, even though growth in exports was still positive at the beginning of the 2010s. From 2010 to 2013, the value added at factor cost in industry fell approximately 20 per cent. Conversely, the value added per hours worked has remained positive, and indicators such as the number of entrepreneurs or skilled labour level have remained relatively stable. In the Tampere Region, human capital and capabilities have remained good, but the development in competitiveness, as measured by production indicators, is currently better described as being stagnant than surging forward.

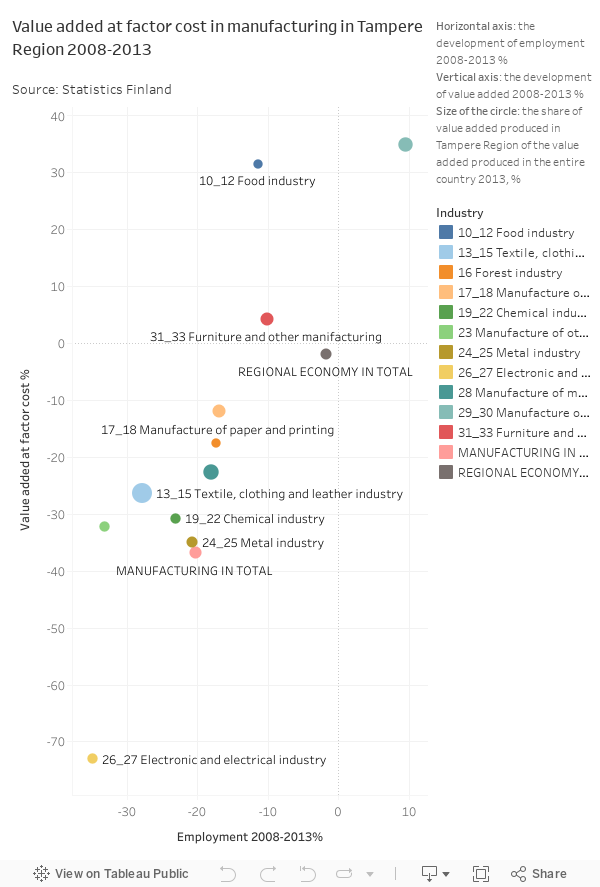

When examining the development of value added at factor cost in industry in the Tampere Region during the period 2008-2013, it can be seen that there was positive value added development in only a few sectors (food industry, automotive industry, furniture and other manufacturing). In all, the value added at factor cost in manufacturing dropped 36.8 per cent from 2008 to 2013, while the drop in value added for the entire Tampere region had remained at 1.9 per cent. In terms of employment, only the number of persons employed in the manufacture of vehicles went up during the period under review. On the other hand, the share of value added at factor cost in manufacturing for the Tampere Region out of the value added at factor cost in manufacturing for the entire country remained quite stable. The share of value added at factor cost in manufacturing rose 1.6 percentage points from 2008 to 2013. In 2013, the Tampere Region's manufacturing industry accounted for 10.3 per cent of the value added at factor costs in manufacturing for the entire country. Correspondingly, it accounted for 8.6 per cent of the entire regional economy.

The importance of the manufacturing industry in the Tampere Region economy from a value added standpoint has, however, seen a significant decline after 2008. In 2008, the manufacturing industry accounted for 31.5 per cent of all value added in the Tampere Region. By 2013, it had dropped to 20.3 per cent. With regard to employment, the change has not been as significant (share in 2008: 22.9 %; share in 2013: 18.6 %).

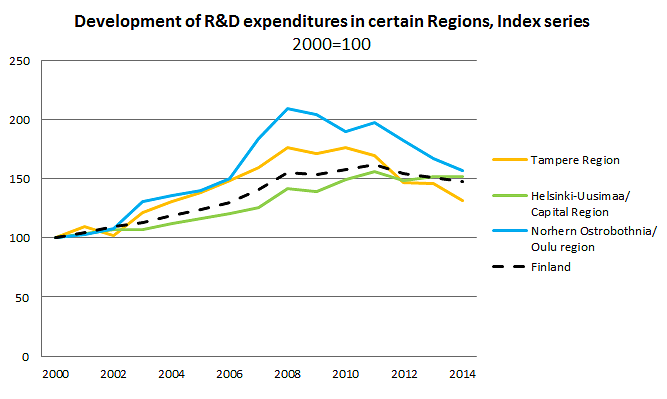

In terms of RDI funding, the trend has been downward in recent years. Although cutbacks in RDI activities is a phenomenon affecting nearly the entire country, the falloff has been steeper in the Tampere Region than Finland as a whole. The Tampere Region, which is profiled as an RDI region, reached its peak in research and development in 2010, when its research and development expenditures were at an all time high. The EUR 1.2 billion in R&D expenditures accounted for 6.9 per cent of the GDP. Three years later, R&D expenditures accounted for only 5.3 per cent of the GDP, and this downward trend can be expected to continue with cuts in R&D spending. However, the 5 percent share of GDP still exceeds, for example, the 3 per cent target set by the EU.

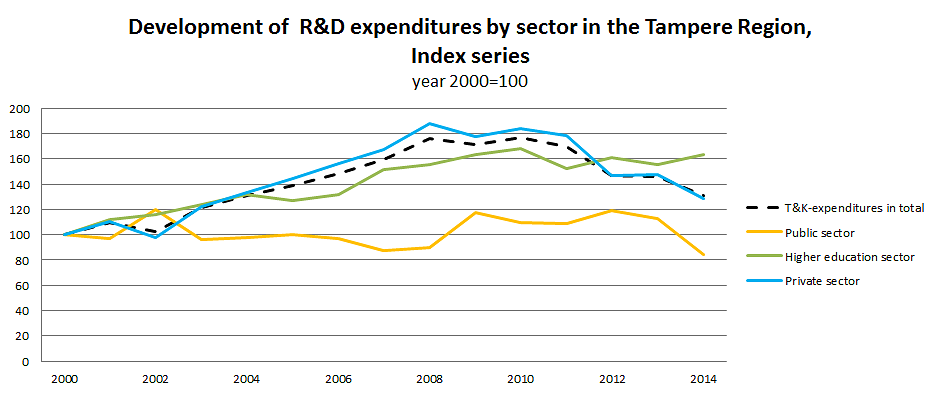

A significant part of this decline is the result of companies cutting their R&D expenses. Company divisions making major RDI investments have left the Tampere Region, which has been unable to attract new RDI contributors to fill the void. As the index analysis of R&D expenditures shown here reveals, private sector R&D activities had a major impact on the entire region's research and development expenditures. The trend lines for HEI and private sector R&D expenditures remained roughly on a par with each other up until 2010, after which the index curves diverged. The level of R&D expenditures in the HEI sector has stayed the same or even risen, while private sector R&D expenditures have taken a rather steep tumble. Even though the developmental trend of R&D expenditures has been negative in the 2010s, the regional R&D intensity is still higher than that of the entire country. In 2014, per capita R&D expenditures in the Tampere region were EUR 1,653/resident, while they were 1,190 €/resident for the rest of the country.

In higher education institutions, investments in research and development have more or less remained the same throughout the 2010s, even though the amount of external funding has decreased and, for example, the amount of Tekes funding going to universities has been reduced. Indicators describing the status of HEIs have remained steady, but major variations can also be found in them. Even though HEI funding indicators have remained largely unchanged, funding seems to be on a downward trend. However, HEIs have adopted a more strategic approach in applying for funding, such as where Academy of Finland funding is concerned. As competition for funding increases, so does the importance of a strategic approach. A constantly increasing share of the research funding for HEIs is external, competitive bid funding. At present, the Tampere3 process, whose aim is to reform the field of higher education in the Tampere Region, offers an opportunity to also increase the level of strategic approach in funding.

HEIs have played a key role in attracting international experts over the past 10 years. The number of new foreign degree students has risen significantly from 2006 to 2012. The number of foreign researchers has also grown during the 2010s. The international attractiveness of the Tampere region has been quite good, but accessibility has declined with the downsizing of operations at the Tampere-Pirkkala Airport. However, the region still maintains excellent connections with the entire country and fast access to the capital region also promotes international attractiveness. Regional accessibility and, in particular, improving international connections have risen to become some of the most crucial areas requiring further development.

The Tampere Region is considered a strong export region. In 2009, just like the rest of the country, the Tampere Region was adversely affected by the international financial crisis. In 2009, exports fell by nearly one-third, dropping from EUR 5.7 billion to EUR 3.9 billion. Since then, Tampere region exports have recovered slowly, even more slowly than average. Even though the Tampere Region trade balance is still higher than the trade balance of the entire country, it has been on a downward trend since 2008. In 2013, there was a momentary increase in the trade balance, but the soft economy pushed it back down the following year. In terms of exports, the Tampere Region is still an industry-intensive region, with industry accounting for 94.9 per cent of all goods exports in 2015. Only North Savo and North Karelia had a higher industrial export share than the Tampere region.

The Tampere Region's innovation platform field has advanced and diversified in recent years. New operators have established themselves in the region and the innovation platform approach has expanded to meet an even wider range of development needs. Taking part in activities provided in a platform is becoming more common among companies as well as individuals. Students and the ICT sector were at the forefront of the platform approach through the New Factory, the nascent platform field is constantly activating new user groups.

The number of growth companies in the Tampere Region has been on an upward trend up to the most recent growth period. From the 2007-2010 growth period to the 2010-2013 growth period, the number of growth companies in the Tampere Region grew nearly 50 per cent. However, the number of growth companies took a downward turn in the most recent growth period. The poor economic situation during the last years has also had an impact on the number of growth companies. The number of patent applications filed in the Tampere Region has declined during the 2010s. Since 2010, the number of applications dropped approximately 42 per cent. The share of applications filed in the Tampere Region out of patent applications filed in the entire country fell from 11.9 per cent in 2010 to 8.7 per cent in 2015. Other indicators for growth companies, such as companies established on innovation platforms or in HEIs or funding aimed at growth companies, are characterised by major fluctuations, which makes their time-based monitoring more wave-like in nature.