23/8/2016 RDI funding workshop

Held at the end of August at the Tampere University of Technology, the workshop dealt with the theme of RDI funding. The workshop was attended by RDI funding experts from, for example, HEIs and other regional organisations. Below are excerpts from the workshop results.

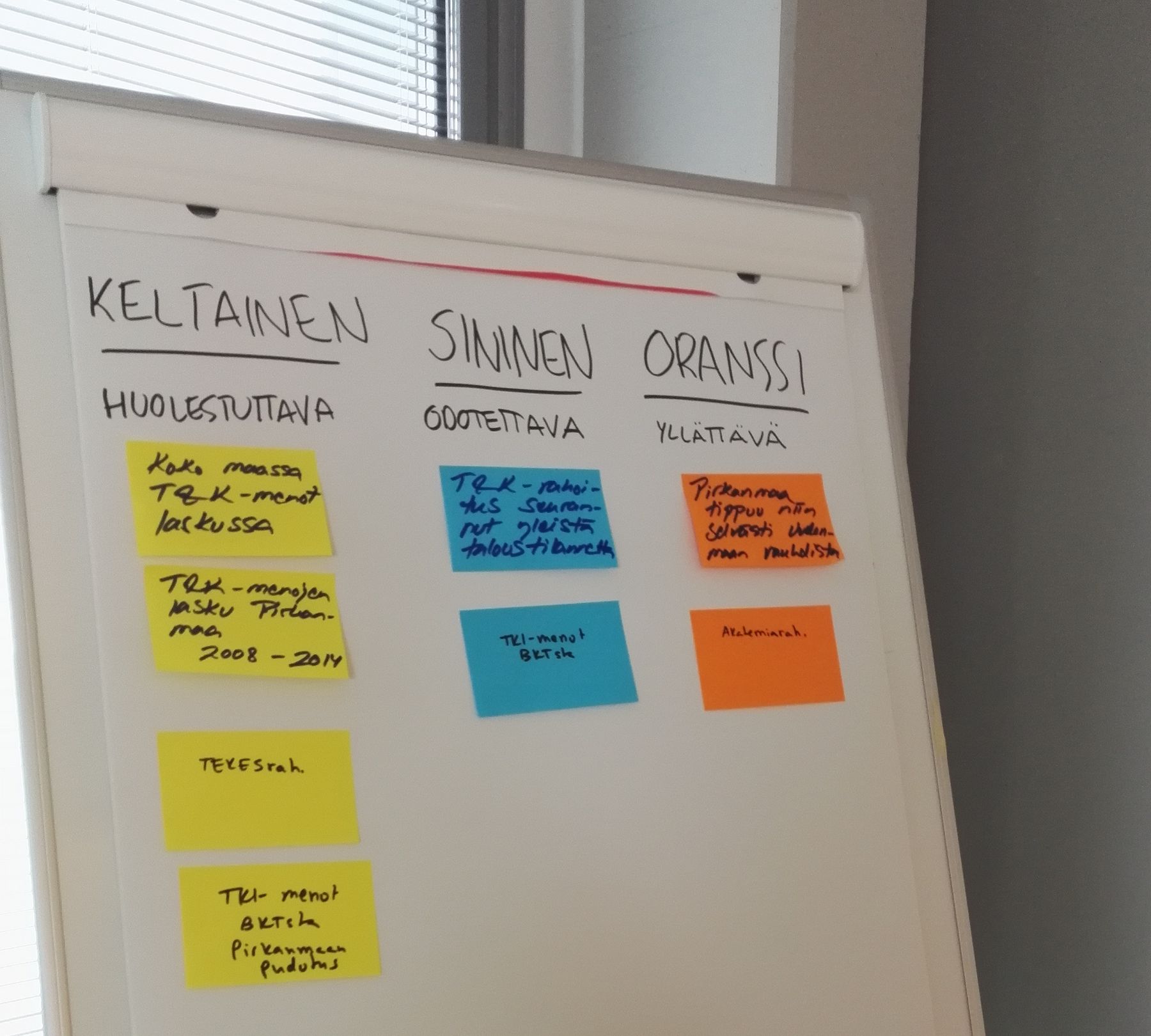

Concerning, expected and surprising findings were taken from the statistical data.

- Surprising: "The Tampere region is falling way behind Uusimaa."

- Expected: "The R&D expenditures have mirrored the general economic trends and its share of the GDP has dropped."

- Concerning: "R&D expenditures are in decline across the country - the trend in the Tampere Region is especially worrying."

Based on the findings made, discussions were continued in other group work tasks.

"The Tampere Region is not as attractive as Uusimaa in the eyes of RDI investors. The Tampere region must be able to hold its own, such as when making decisions on new investments."

"The areas of strength and expertise in the Tampere Region have not generated any additional funding for the region. The strengths should act as magnets for bringing investments. The lack of a systematic approach might also be a reason for the lack of investments. We would need something like an industrial reform programme to enhance our strategic approach."

"Ensuring the level of RDI funding demands a more strategic approach to funding applications. Closer co-operation and focusing on more influential entities can promote the enhancement of a strategic approach."

"Do we need to change our mindset where the whole region is concerned? A common mindset must be established in order to ensure that different actors in the region are working toward achieving the same goals."

"The Tampere Region must give thought to what new things can be created and drawn from our existing strengths."

"The traditional role of RDI is changing with the rise of an experimental culture: new things are being increasingly created in non-RDI activities."

"The Tampere Region's new RDI profile also requires a change in culture as well as learning how to work under the new operating conditions."

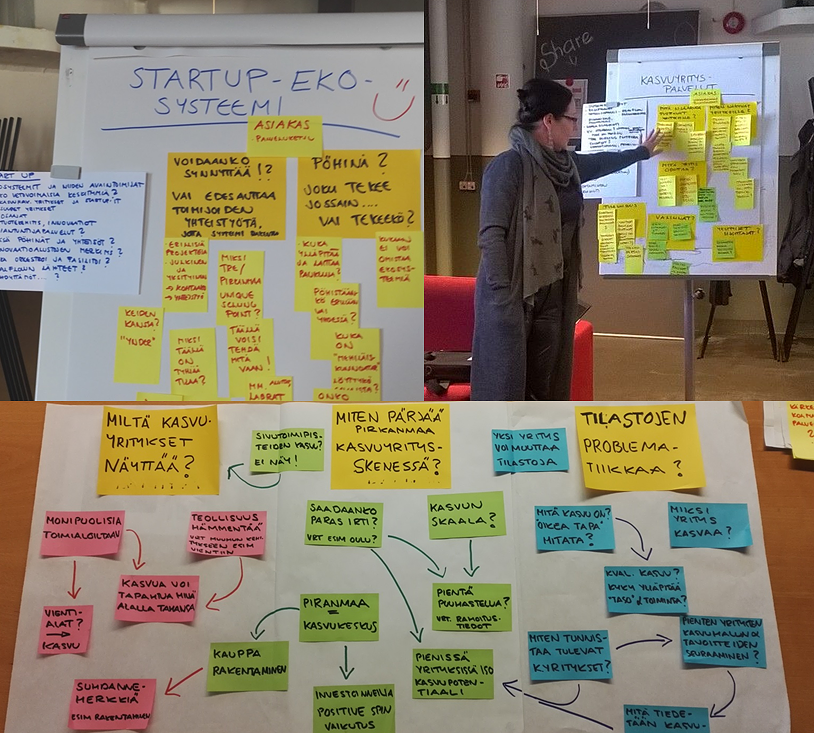

8/9/2016 Growth companies and startups in the Tampere Region workshop

Views on the growth companies and startups in the Tampere Region were reviewed at the New Factory in the beginning of September. The event was attended by, for example, representatives from businesses and business services as well as sources of public and private enterprise funding. The event was organised by the Council of Tampere Region along with the New Factory and Tredea.

At the workshop's learning café tables, participants worked with the following themes, making the following observations on them:

Growth company services

- Advisory board – The right advisors for the right situations.

- Simplifying enterprise services.

- Are there unnessecary thresholds? Is there a sufficiently low threshold for making contact and discussing things?

- Grassroots-level assistance and familiar contact persons.

- How can a growth attitude be supported?

Growth company measures - "small steps"

- Courage to think big: Company-on-company sparring. Should we mimic the Swedish business attitude? What would Börje do?

- Crossing death valleys: Tales of survival along with success stories. Crisis service for entrepreneurs and "early warning" monitoring.

- Improving funding planning and application expertise: education about valuation and raising financial awareness. A new type of growth camp "required by funders".

- Improving product expertise and service design: purchasability sparring service. Training in productisation and service design.

Growth companies behind the statistics

- Although the risk-taking threshold for small enterprises is high, they might have growth potential. On the other hand, even though an enterprise would be confident and ready to take a risk, can confidence be found elsewhere?

- Growth is possible in any sector. Avoid getting locked into certain expectations.

- Investments can also have a positive impact on enterprise growth.

- Continuous improvement: what happens to enterprises after the growth period?

- Is growth in the number of employees the most appropriate way to measure growth? How do, for example, the platform economy and network-type business affect measurement?

- How can growth enterprises really be identified and what unites them other than success?

- Can the highest possible growth potential be realised in the Tampere Region?

- How can the growth-orientation and goals of small enterprises be monitored?

Startup ecosystem

- What makes the Tampere Region a "unique selling point"?

- We need systematic work!

- Up with “Founded in Tampere” (cf. “Founded in Groningen”)

- Peer support and sharing from startups.

- Who is the queen bee of the startup ecosystem? Is one overall needed?

- Are there enough "buzz" processes here? Are we buzzing around together or separately?

Large companies in the startup scene

- Who actually has an overall understanding? For example, is it known how many corporate venturing investments are being made in the Tampere Region or who is making them?

- There is, however, a buzz in the air regarding this. Investments are made in startups and deals are made with them, they are purchased and internal startups are also established and merged into a corporation or spun off.

- There is a need for activating the field, such as with regard to spin-offs.